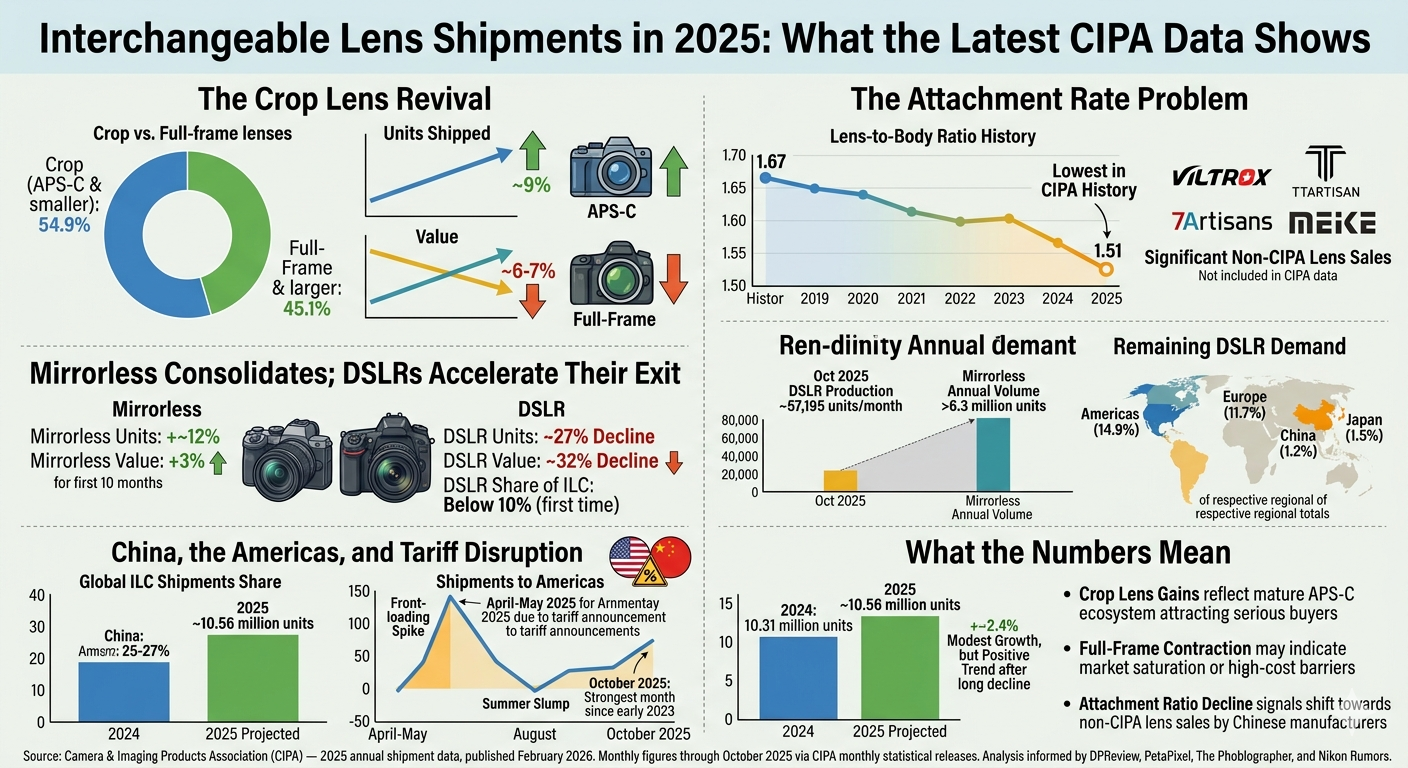

The infographic is summarizing the 2025 CIPA data for interchangeable lens shipments. Here is a breakdown of the key findings illustrated in the image:

The Crop Lens Revival: Data shows that APS-C and smaller sensor lenses accounted for 54.9% of shipments. While this segment saw growth in units (up 9%) and value, full-frame lenses experienced a decline in both.

The Attachment Rate Problem: The lens-to-body ratio fell to a record low of 1.51 in 2025. This section notes the rise of non-CIPA manufacturers, like Viltrox and TTArtisan, whose sales are not captured in these official statistics.

Mirrorless vs. DSLR: The transition to mirrorless is nearly complete. Mirrorless units and value saw growth, while the DSLR segment declined sharply by approximately 30% in both categories, dropping below 10% of the market share. The map shows that remaining DSLR demand is concentrated in the Americas and Europe.

Tariff Disruption: A major spike in shipments to the Americas occurred in April-May 2025 in response to tariff announcements, followed by a summer slump and recovery in October.

Overall Market Outlook: The total market shows modest growth (up 2.4%) from 2024 to 2025, reaching an estimated 10.56 million units. The decline in the attachment ratio remains the most important trend to watch.