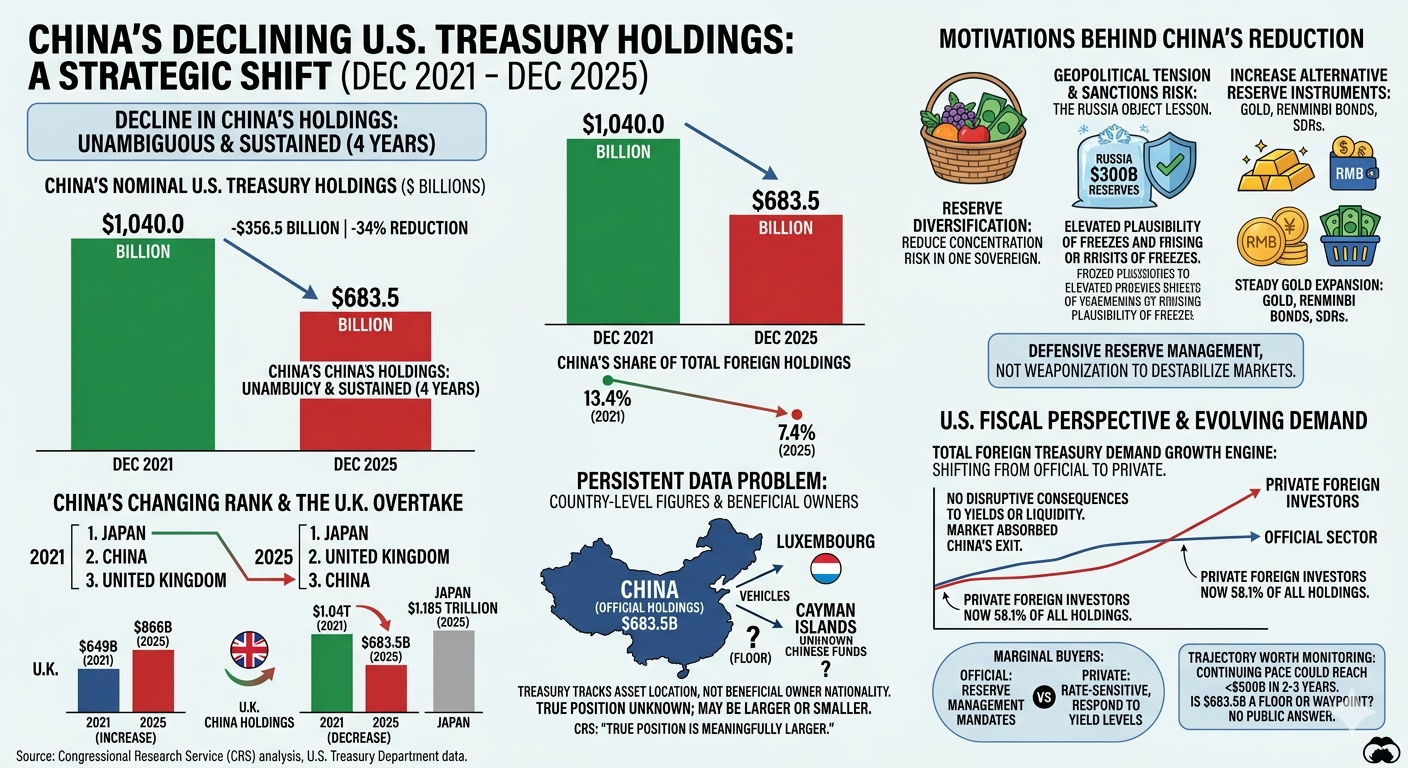

This infographic illustrates the significant shift in China’s holdings of U.S. Treasury securities over the four-year period from December 2021 to December 2025.

Executive Summary: The Great Repositioning

China has executed an unambiguous and sustained reduction in its exposure to U.S. federal debt. While China remains a top-tier creditor, the data shows a clear pivot toward reserve diversification and risk mitigation.

Key Data Points (2021–2025)

| Metric | December 2021 | December 2025 | Change |

|---|---|---|---|

| China’s Nominal Holdings | $1.04 Trillion | $683.5 Billion | −$356.5 Billion (−34%) |

| Share of Foreign Holdings | 13.4% | 7.4% | −6.0% Total Share |

| Global Rank | 2nd Place | 3rd Place | Overtaken by UK |

The Rank-Order Shift

While Japan remains the largest foreign holder (at roughly $1.185 trillion), the United Kingdom has ascended to the second spot. UK holdings grew from $649 billion to $866 billion during this interval, contrasting sharply with China’s exit.

Strategic Motivations

China’s reduction is widely viewed as defensive reserve management rather than an attempt to “weaponize” debt.

- The “Russia Lesson”: Following the 2022 invasion of Ukraine, Western governments immobilized approximately $300 billion in Russian central bank reserves. This highlighted the geopolitical risk of holding assets in a single foreign sovereign’s paper.

- Diversification: To lower vulnerability to sanctions or asset freezes, China has steadily expanded its gold reserves and alternative instruments like renminbi-denominated bonds.

- Asset Location vs. Ownership: It is important to note that Treasury data tracks where the asset is located, not the nationality of the owner. Because Chinese entities often invest through vehicles in the Cayman Islands or Luxembourg, the $683.5 billion figure is considered a floor, not a ceiling.

Market Implications

Contrary to “doom-and-gloom” predictions, China’s gradual exit did not disrupt U.S. Treasury yields or liquidity.

- Private Sector Surge: The growth engine of Treasury demand has shifted from foreign governments to private foreign investors, who now account for 58.1% of all foreign holdings.

- Rate Sensitivity: These private buyers are more sensitive to interest rates and yields than to geopolitical mandates, changing the marginal buyer dynamics for U.S. debt.

Future Outlook

If the current trajectory continues, China’s holdings could dip below $500 billion within the next two to three years. The primary question remains whether this represents a total exit or a strategic rebalancing to a new “floor” of integration.